You need a budget. Lessons I learned from the number one book on how to budget.

In this article, I will share the practical lessons I have learned from reading the book "You Need a Budget". The book outlines four rules that can guide you in budgeting as a Ugandan, and this article will be based on those rules. Spoiler alert, rule 4 is the most important

Before we dive into the rules, there is something essential that you need to know. Instead of planning for future money, you should budget for what you currently have in your bank account. Don't budget for what you hope to receive after a salary raise or any unexpected income. Look at the balance you have in your bank account or the cash you have at hand and plan accordingly.

Don't budget money you don't have.

Rule #1: Give every dollar a job

To give every dollar a job means that when you have money in your bank account, you should budget for it by defining what each dollar will do. To do this, you need to find things you want your money to do for you and prioritize them. You can do this by asking the question

What do i want my money to do for me?

You answer this by listing your priorities and allocating money to them. The necessities need to be covered first. These include things like rent, food, and transportation to work. After these necessities are covered, you can allocate money to other items in decreasing order of priority.

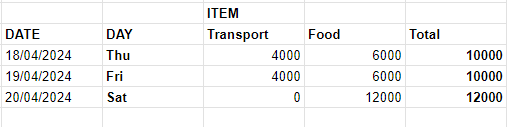

For example, let's say you have UGX 100,000 left in your bank account, and your immediate needs are transportation to work and feeding for the rest of the month until your next paycheck. You would calculate how much transport and food you would need for the rest of the month and then draw up a table that looks like the one below to allocate the remaining money to these categories for the rest of the month.

But, what if the money you have is not enough to survive until your next paycheck? In that case, you have a few options. 1. You can either squeeze your budget further and only allocate each category the bare minimum, 2. try to find another source of income in the short term, or as a last resort, 3. Get a small loan from a friend that you can pay back when you receive your next paycheck.

Rule #2: Embrace your true expenses

Rule two exists to help you with those expenses that catch you by surprise when you're out of money. It's all about breaking down big expenses and planning for them each month.

Rule 2 is specifically for infrequent expenses - expenses that don't happen every day or every month. These could be things like Christmas holidays or replacing your car tires. There are two types of infrequent expenses: predictable and unpredictable but inevitable.

Predictable expenses are those that happen infrequently, but we know when they will happen. For example, Christmas expenses, birthday expenses, or car services.

Unpredictable but inevitable expenses are those that we cannot predict when they will happen, but they will happen soon enough. For instance, contributing to a wedding or needing new clothing for a last-minute event.

The best way to prepare for all kinds of expenses is to allocate a portion of your income towards them. By doing so, you'll be more prepared to take care of them when they occur. This creates a pool of money that will always be there waiting for these expenses to happen. In essence, this serves as an emergency fund, but it's more directed towards these specific expenses.

Our app offers the option to save towards specific goals, such as saving a fixed amount every month towards a particular target, like Christmas expenses. Give it a try! Try out the PesaSave app

So that's all about Rule 2. Break down big upcoming expenditures and allocate money towards them every month. This will make them more achievable

Rule #3: Roll with the punches

The phrase "roll with the punches" may sound exaggerated, but it summarizes what rule 3 is all about. You make a plan, but unexpected expenses can come up and you have to adjust your plan accordingly. In other words, the rule is about modifying your budget.

No matter how well you plan, you will encounter surprise expenses. For example, your car may break down and require repair, or a family member may have an urgent need. You need to adjust your budget to accommodate such expenses. However, this does not mean that you should abandon your budget entirely. Certain expenses are non-negotiable and must be paid, even if they were not planned for. The purpose of a budget is to help us manage our finances, and if it cannot be adjusted, then it is not serving its purpose. When you do make changes to your budget, make sure to remove dollars from one category and allocate them to the new expense.

If you find yourself frequently adjusting your budget, it may be a sign that you did not use rule one effectively when allocating your dollars to budget items.

Remember: Changing your budget is not a failure. If things do not go as planned, just roll with the punches and keep going.

Rule #4: Age Your Money.

This is the most important rule of personal finance, and if you have to choose only one rule, it should be this one: Age your money.

In simple terms, aging your money means knowing how long the money you have in your bank account will last. It's not just about having a lot of money in your account, but rather about how long that money has been sitting there and how long you expect it to last.

Rule four is about getting to a point where you don't need your next paycheck.

Let's say you have a water tank with an inlet at the top and an outlet at the bottom. The inlet is used to add water, while the outlet is used to take out water. If you take out water faster than the rate at which the tank gets filled, the tank will eventually run out, and that's not a big deal if you have other tanks of water, but it is a very big deal if the only water tank you have is running empty.

The best way to avoid running out of water is to take out less than what is added each day. When this happens, the leftover water slowly builds up, and you might never run out of water. But if you take out all the water that is filled each day, you're living on the edge, because you'll run out even if the tank is not refilled for even a single day.

If you're taking out 7-day-old water, it means you have a 7-day window (buffer) between the time the water is added and the time when you will need it. The bigger the gap, the better, and you will have more flexibility even if something unexpected happens.

And that's the goal of rule four: to help you measure how old your money is. Look at the water tank as your bank account, the water inlet as your income, and the outlet as your expenses. If you're spending the money you earned on Monday on a Tuesday, your money is one day old. If you're spending it on a Friday, your money is 5 days old, and this means you're living paycheck to paycheck if you're spending money you earned yesterday or this week.

The older your money is, the better, and having a 30-day window between when you receive money is not only recommended but better than living paycheck to paycheck.

Conclusion

By following these 4 budgeting rules and practising them for at least 3 months, you are bound to keep your financial life in order and stop worrying about money. You can read more about these rules in the You Need a budget(YNAB) book. Also, if you love articles like this one, please consider subscribing to our newsletter. We publish similar articles once a week.